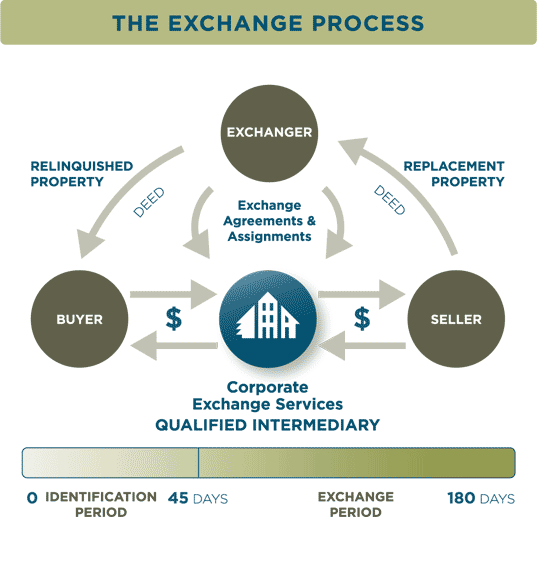

Party who enters into the Exchange Agreement with the Taxpayer, acquires the Relinquished Property from the Taxpayer, transfers the Relinquished Property to the Buyer, invests the proceeds from the transfer of the Relinquished Property, acquires the Replacement Property from the Seller, and transfers the Replacement Property to the Taxpayer.